Uncertain times for the UK Economy

According to the World Economic Forum's Global Competitiveness Report 2019, the UK is the world's 9th most competitive economy (out of 141 countries surveyed). The UK economy is highly developed, liberalised and globally integrated and London’s financial centre has long been a strong driver of economic growth, helping the UK to outperform most other G7 economies in the ten years to 2007. However, the 2008 international financial crisis turned the reliance on banking and related services into a vulnerability, now emphasised by the British departure from the EU.

Dun & Bradstreet has downgraded the UK's country risk rating several times since the Brexit referendum in 2016 and it now stands at a new all-time low, reflecting the adverse impact of the coronavirus pandemic on opportunities for both traders and investors. The economic damage caused by the current lockdown in the UK is likely to be immense. Large parts of the economy, including hospitality, leisure, entertainment, retail (except supermarkets) and transport are now closed, while other sectors - such as manufacturing are suffering from supply chain disruption and a lack of workers as schools are shut. Taking all factors into account, Dun & Bradstreet is lowering its real GDP growth forecast for 2020 from 0.8% to now -2.5%. While a recovery in the second half of 2020 and in 2021 seems likely, the magnitude of this will largely depend on the success of the global containment efforts. Either way, the UK will almost certainly enter a technical recession in Q2 2020, and real GDP growth for the year as a whole is likely to be worse than during the financial crisis.

Reacting to the Economic Impact of Coronavirus

Business leaders and economists had long been pondering the timing of the next recession and its most likely triggers. Unfortunately, no-one could predict nor prepare for the destructive capacity of the coronavirus (COVID-19) pandemic: exogenous factors such as epidemics/pandemics are difficult to model or control – you can only respond as best you can.

In response to the virus outbreak, the central banks of the US, the euro zone, and the UK were quick to take action, lowering short-term interest rates and or increasing the size of their Quantitative Easing programmes. After two weeks, as evidence mounted that the crisis was snowballing, authorities in the world’s largest economies announced stimulus packages, which included unprecedented interventions such as extensions to statutory sick page and temporary ‘furloughing’ of employees with the government paying 80% of wages for a temporary period. Even with governments ready to infuse billions to trillions into their economies, the overall uncertainty is driving volatility in the major equity exchanges worldwide and there is a real risk of rising unemployment and business failures.

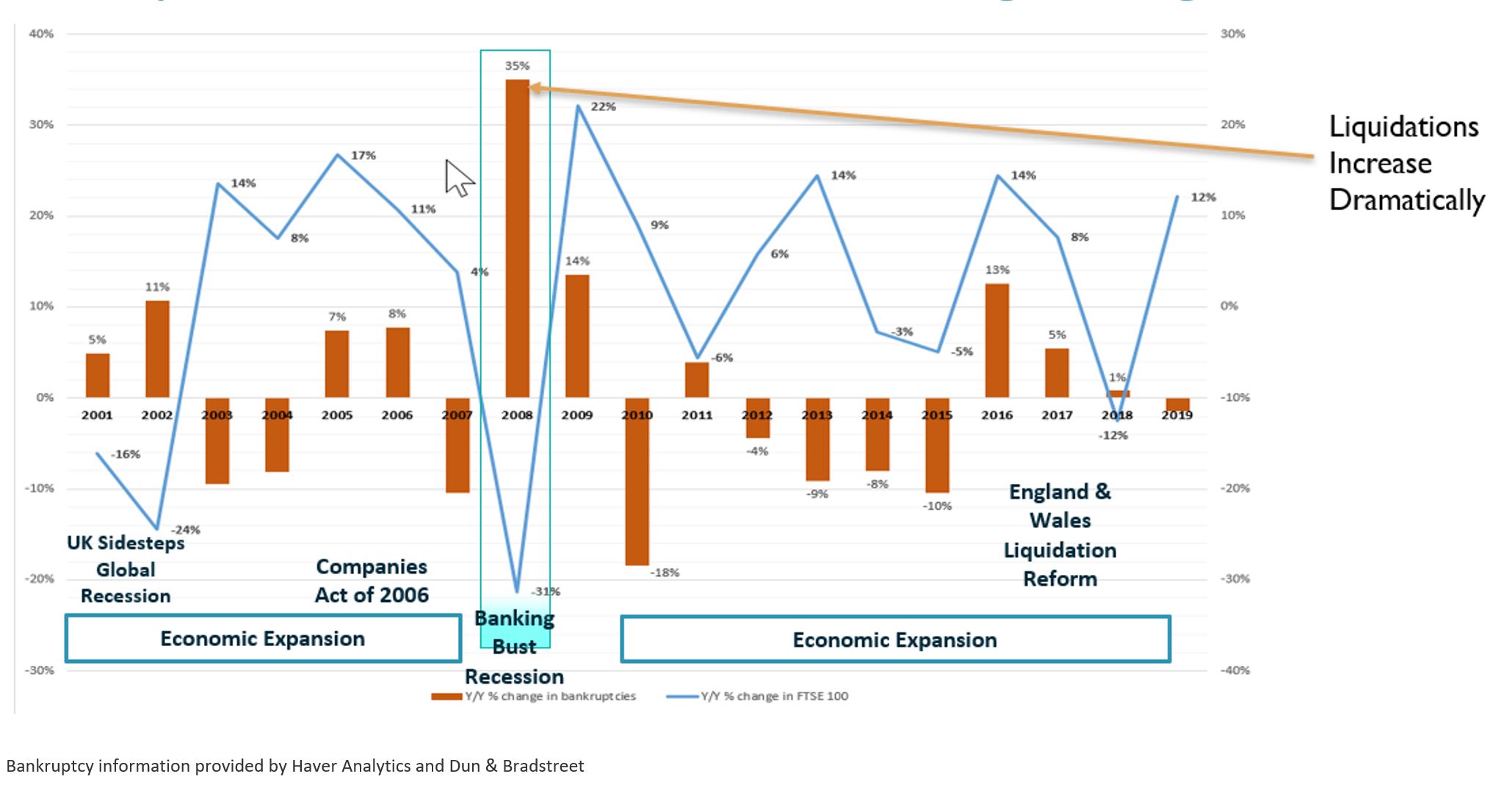

Correlation Between Recessions and Bankruptcies

Dun & Bradstreet is tracking these developments in the world economy very closely. Our analysis shows four years of year-over-year increases in UK liquidations since 2001: two of these increases are directly related to economic cycles/recessions, while the other two could be related to changes in business and liquidation laws:

1. Liquidations Related to Recessions:

Global Recession of 2001-02

- UK year-over-year liquidations increased by +16% and the FTSE100 dropped by -40%

- The UK managed to maintain GDP growth and avoid the wider recession.

The Banking Crisis and Economic Recession of 2008-09

- During this global recession UK liquidations increased by +49% and the FTSE100 dropped by -31%.

The UK rolled out changes in business and liquidation laws in both 2006 and 2017. During these roll-outs bankruptcies increased both in the year before the change and in the year of actual implementation. Though there were some pockets of UK economic weakness in 2005 (consumer spending and the housing market faltered), these factors might not account for two years of consecutive increases in bankruptcy counts.

UK Liquidations and FTSE100 Performance Diverge During Recessions

"Central banks are taking strong actions to counter the impact of coronavirus. These precautions could help financially-secure companies that require a short-term liquidity solution, but, as we saw in 2008, companies in a weak financial state are at an increased risk of failure and could fail. Given 10+ years of expansionary business creation and low bankruptcy rates, we are concerned that an economic downturn could result in an unprecedented number of liquidations," Markus Kuger, Chief Economist for Dun & Bradstreet, said.

How to Prepare for Potential Impacts to Global Business Credit

I’m advising my finance and credit clients to re-evaluate their company’s credit policies to ensure they are:

- Onboarding an Appropriate Balance of Risk – Reassess your company’s credit policy to recalibrate the portfolio risk profile for new and existing customers to an approach that is more appropriate for a recessionary economy.

- Setting Proper Credit Limits – Use this opportunity to realign credit limits. Make sure they are informed by the credit exposure you have for the entire global corporate hierarchy for that customer. Consider adjusting credit limits (up and down) based on the individual risk assessment of that customer.

- Establishing Appropriate Credit Terms and Conditions – Evaluating the potential risk of each new opportunity or customer renewal will help realign your credit terms based on the probability the customer will pay on time and within terms.

- Monitoring Portfolio Risk – Perhaps more urgently, consider deploying credit risk monitoring of the entire global portfolio to pick up on pockets of weakness that could result in bad debt losses from potential bankruptcies.

There are opportunities in every economic situation. Many companies may need to quickly acknowledge that bad debt losses have been muted over the past 10 years. We could be entering a new economic reality that requires a more active approach to credit risk mitigation.

Let Dun & Bradstreet help you understand the hidden risk in your customer portfolio through the D&B Customer Risk Health Scan. This complimentary report identifies which of your customers are in geographies, industries or corporate families that are significantly impacted by coronavirus, or were already showing signs of financial stress prior to the outbreak.