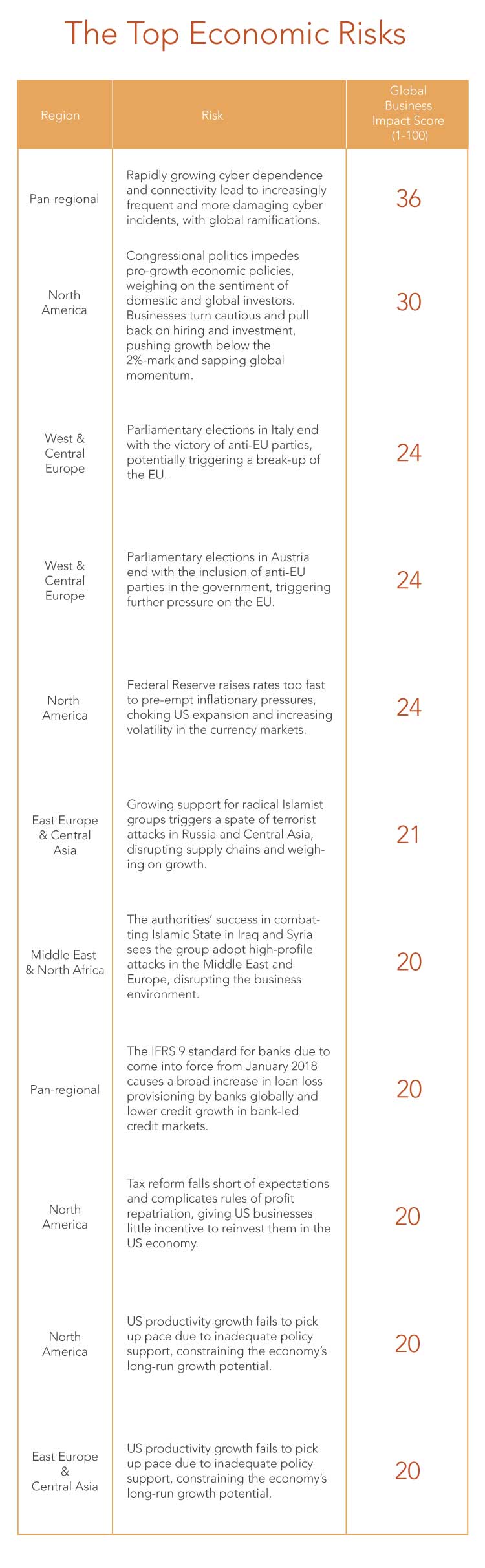

Ten Key Risks for Businesses in a Global Economy

The Dun & Bradstreet Global Risk Matrix ranks the biggest threats to business based on each risk scenario’s potential impact on companies, assigning a score to each risk. The scores from the top ten risks are used to calculate an overall Global Business Impact score.

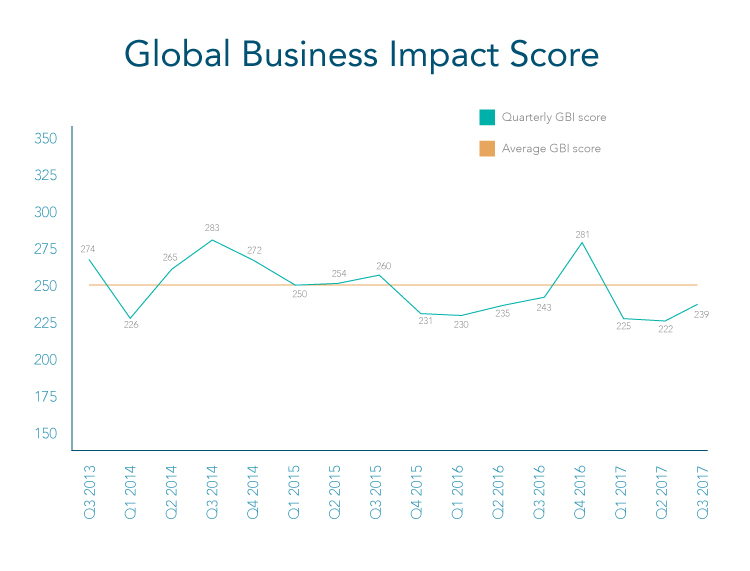

Our latest Global Business Impact score highlights a deteriorating risk outlook for cross-border businesses. This reverses the improving trend seen in the previous two quarters, but – importantly – the score is still better than the long-term average.

Risks Increase for the First Time This Year

Dun & Bradstreet’s Global Business Impact (GBI) score for Q3 2017 recorded an increase from last quarter’s all-time low, climbing from 222 (out of a maximum of 1,000) in Q2 to 239, indicating a deterioration in the global business operating environment. But the Q3 score is a significant improvement on the position at end-2016, when it reached an almost-record high of 281; the Q3 outcome is also well below the long-term average of 249.4.

The latest score confirms our view that business conditions, although still feeling the after-effects of the global financial crisis, have been able to cope with uncertainty caused by the unexpectedly dramatic political events in 2016 – such as the UK’s vote to leave the EU and the election of Donald Trump as US president. However, risks associated with political and security concerns, and with US economic policy, have increased in Q3, pushing the score upwards.

Our top ten risks combine an assessment of: (i) the magnitude of the event’s probable effect on the global business operating environment, on a scale of 1 to 5 (where 1 is the smallest impact and 5 is the largest); and (ii) the likelihood of the event happening.

Five New Risks in the Global Top 10

The Q3 2017 GRM has five new entries: three are from North America, one from West and Central Europe, and one from Eastern Europe and Central Asia. This geographic spread shows that finance, procurement and supply chain teams across all business sectors face urgent and ever-evolving risks in an increasingly complex and globalised world. The five new-entry risks are:

- US Congressional politics impeding pro-growth economic policies (GBI 30, out of a maximum 100); (GBI 30, out of a maximum 100);

- Parliamentary elections in Austria ending with the inclusion of anti-EU parties in the government, triggering further pressure on the EU (GBI of 24);

- Growing support for radical Islamist groups in Eastern Europe and Central Asia (EECA) triggering a spate of a terrorist attacks in Russia and Central Asia, disrupting supply chains and weighing on growth (21);

- US tax reform falling short of expectations, slowing US/global growth (20); and

- Slow US productivity growth constraining growth potential (20).

Among our pre-existing risks, we have increased the likelihood (from 70% to 90%) of the risk from damaging cyber incidents with global ramifications; this has increased the GBI from 28 to 36 (out of 100). We have also increased the likelihood (from 30% to 33.3%) of persistent economic hardship and growing frustration with government policies and corruption triggering ‘colour’ revolutions in the EECA region. This has resulted in the GBI increasing from 18 to 20. We have also increased the global impact from 2 to 3 (out a maximum 5) of the US Federal Reserve raising interest rates too fast, hindering US expansion and increasing volatility in the currency markets; consequently, the GBI here increased from 16 to 24. The remaining two risks saw no change in their GBI scores from Q2 2017.

Global Business Impact Score

US Policy’s Importance to Global Business

The Global Risk Matrix for Q3 2017 highlights the importance of the US economy and, in particular, policy-makers in Washington to the continuing global recovery, with four of our top ten risks emanating from the US. Three of these are new entries.

The first of the risks, emanating from North America, is in second place in the Global Risk Matrix with a GBI of 30. We are concerned that Congressional politics will impede pro-growth economic policies, weighing on the sentiment of domestic and global investors. As a result, businesses will turn cautious and rethink their hiring and investment strategies, which would push growth below the 2%-mark and sapping global momentum.

In equal third place is the worry that the US Federal Reserve raises interest rates too fast in an attempt to pre-empt inflationary pressures, stalling US expansion and increasing volatility in global currency markets and, by extension, growth prospects. This risk has a GBI of 24, up from 16 in the previous report.

In equal seventh place with a GBI of 20 are two further risks emanating from North America. There is a possibility that US tax reform will fall short of expectations and complicate rules of profit repatriation, giving US businesses little incentive to re-invest these profits into the US economy, slowing both US and global growth. Finally, there is concern that if US productivity growth fails to pick up pace, due to inadequate policy support, it will constrain the economy’s long-run growth potential.

Security Concerns Elevate

Security concerns also feature heavily in this quarter’s Global Risk Matrix. Four such risks are highlighted, including our number one risk, with a GBI of 36 (up from 28 and second place in Q2 2017). A number of high-profile cyber attacks in 2017 confirm that the rapidly growing problem of cyber dependence and connectivity is set to lead to increasingly frequent and more damaging cyber-security issues, with ramifications for doing business. This is the only pan-regional risk in the current GRM.

The second and third security concerns relate to radical Islamist groups. In sixth place overall, with a GBI of 21, is the worry that growing support for radical Islamist groups in the EECA region triggers a spate of terrorist attacks in Russia and Central Asia, disrupting supply chains and weighing on growth. Relatedly, in equal seventh place, with a GBI of 20, is the risk that military success in combatting Islamic State in Iraq and Syria sees the group adopt high-profile attacks in the Middle East, North Africa and Europe, disrupting the business environment.

Our final security-related concern is that persistent economic hardship and growing frustration with government policies and corruption in EECA triggers revolutions in the region, leading to the collapse of political regimes. The resultant chaos would impact negatively on supply chains and the global business environment.

European Politics and Global Risks

The final two risks in the Q3 GRM, both in equal third place with a GBI of 24, highlight the current importance of politics in the EU. The first risk, which also featured in our previous report, is that parliamentary elections in Italy in February 2018 result in a victory for anti-EU parties. This would increase doubts about the viability of the euro and throw into question the EU’s ability to survive, in turn triggering huge uncertainty over cross-border business with the EU (and indeed for such business within the bloc itself).

The second risk associated with Western and Central Europe is a new entry. There is a possibility that parliamentary elections in Austria in October 2017 end with the inclusion of anti-EU parties in the government, again raising questions about the viability of the EU. However, the EU (and the euro) could survive an Austrian exit, which would not be the case if Italy was to pull out of the euro and/or bloc.

Summary: Business Environment Deteriorates But is Better Than Long-Term Average

The Dun & Bradstreet Global Business Impact score for Q3 2017 shows that risks facing businesses have increased, following improvements in the two previous quarters that saw risk at its lowest level since the GRM started. However, risk is still lower than the long-term average, indicating that businesses have overcome the high levels of uncertainty caused by the Brexit and Trump votes in 2016. Nevertheless, politics, security and policy-making concerns weigh heavily on the business environment, which remains challenging, and business decision-makers need to be aware of the rapidly-changing risk environment.